Global: Trump’s tariff quake is sending shockwaves through economies worldwide

A temporary rebound in manufacturing has recently supported global growth; Fading front-loaded demand and tariff shocks pose a risk to the outlook

US: Reciprocal tariffs heighten the risks of stagflation and recession; despite de-escalating trade tensions, economic slowdown appears inevitable; three rate cuts expected this year

Trump’s tariff tremors would weigh on the global economy, led by US losses, with ASEAN growth set to worsen under reciprocal tariff measures

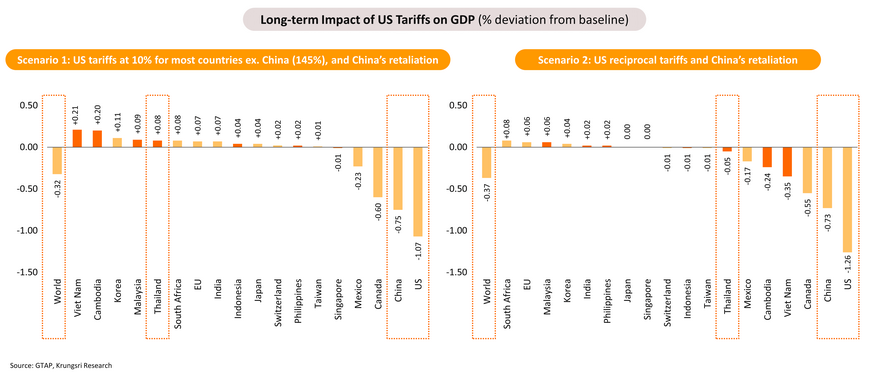

Scenario 1: US imposes a 10% tariff on most countries and a 145% tariff on China. China retaliates with a 125% tariff on US goods.

Scenario 2: US imposes the announced reciprocal tariffs on many countries and a 145% tariff on China. China retaliates with a 125% tariff on US goods.

Eurozone: Impact of fiscal stimulus measures is expected to become more evident next year, while trade war risks remain a key drag on the region’s economic growth

Japan: Consumption remains suppressed by high inflation, while Trump’s trade policy adds uncertainty to the recovery path

China: Additional adrenaline jabs needed as economy continues to struggle from within while fighting trade wars from outside

Thailand: Twin shocks from domestic quake and tariff tremors rattle economic outlook

-

We are set to lower our 2025 GDP forecast from 2.7%, amid mounting economic pressure from the March earthquake and the US tariff hikes.

-

The March earthquake may cause temporary disruptions to some key growth drivers, with economic losses estimated at 0.1-0.2% of GDP.

-

Earthquake, slow Chinese tourist recovery, and other headwinds may drag our forecast of 2025 foreign arrivals to 36-37 million.

-

In addition, Thailand faces potential economic strain from unexpectedly high reciprocal tariffs, intensified by its significant dependence on US markets.

-

High-impact sectors from US tariff hikes include processed seafood, tires, HDDs, electrical appliances, and rubber gloves, while moderate-impact industries comprise rubber, rice, motorcycles, auto parts, jewelry, textiles, plastics, other medical devices, and iron and steel products.

-

Our 2025 Thai GDP growth forecast would soften to a) 2.2-2.4% under a 10% US tariff, b) 1.9-2.1% with US reciprocal tariffs for 3-6 months, and c) to 1.5-1.8% with reciprocal tariffs for over 6 months or if Thailand faces relatively higher tariffs than competitors.

-

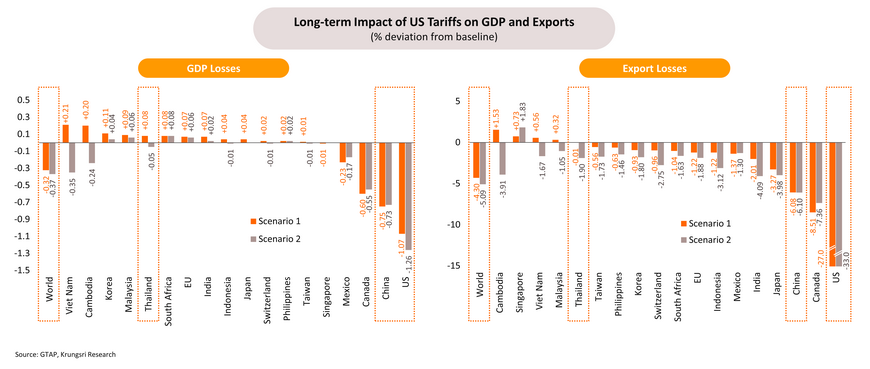

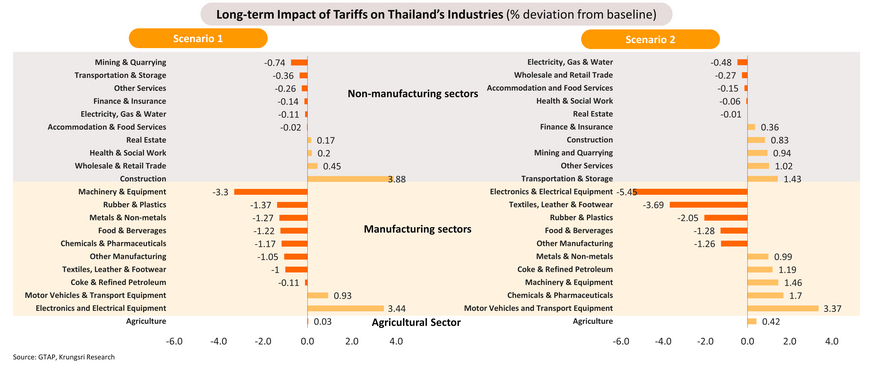

In the long term, the US and the global economy are expected to face the largest GDP and export losses from tariff hikes. ASEAN, including Thailand, would suffer net losses if reciprocal tariffs are imposed. Most Thai industries face losses from tariff hikes. Some sectors see slight gains from the substitution effect, investment relocation, or export rerouting amid rising Chinese imports.

-

Regarding the policy rate, the BOT assesses that current US tariffs affect 'some' sectors, necessitating supply-side policies. This increases the likelihood of a dovish hold in April. However, the growing impact of tariffs raises the chance of a rate cut in 2H25.

Thailand’s already-weak recovery faces heightened challenges from two unforeseen shocks -- March earthquake and US reciprocal tariffs

Earthquake may cause temporary disruptions to some key growth drivers, with economic losses estimated at 0.1-0.2% of GDP

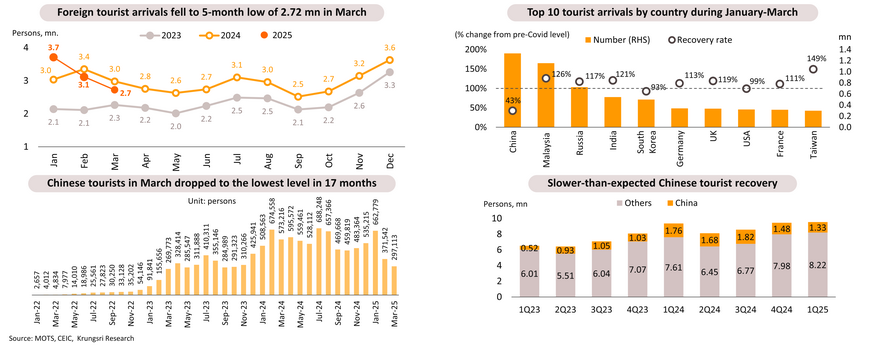

Foreign tourist arrivals this year are preliminarily estimated to be lower than the previous forecast by 1-1.5 million, affected by the Earthquake, safety concerns, and stiff competition

Earthquake, slow Chinese tourist recovery, and other headwinds may drag our forecast of 2025 foreign arrivals to 36-37 million

In March 2025, Thailand welcomed 2.72 mn foreign tourists, the lowest in five months and an -8.8% YoY decline, compared to 3.12 mn in February. Tourism revenue stood at THB 132 bn, down 2.8% YoY. During January-March, total foreign tourist arrivals reached 9.55 mn (+1.9% YoY), generating THB 463 bn (+1.8% YoY). Chinese tourist recovery remains slower than expected, with March arrivals dropping to a 17-month low of 297,113 (-48.2% YoY), totaling 1.33 mn for the first quarter of this year (-24.2% YoY), mainly due to safety concerns and competition from other destinations. Moreover, the earthquake that occurred in late March may negatively impact the tourism recovery outlook, particularly slowing down the already sluggish recovery of Chinese tourists. As a result, the overall number of foreign tourist arrivals this year is at risk of falling short of the previously projected 38 mn and may be in the range of 36-37 mn.

While the March Earthquake may slow foreign tourist arrivals in Q2, the impact is expected to be limited in the short term based on historical data

Under Trump’s second presidency, a series of tariff hikes would intensify trade wars, potentially affecting global trade and economies, including Thailand

Thailand and ASEAN may face economic strain from higher-than-expected reciprocal tariffs, compounded by their heavy reliance on US markets

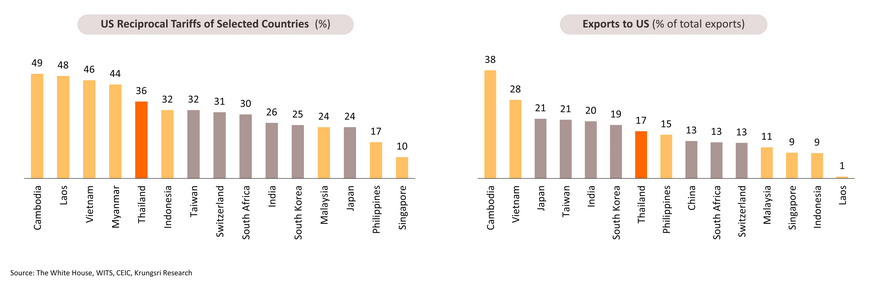

US President Donald Trump announced the implementation of universal tariffs, including a 10% import duty on most goods, starting April 5. The reciprocal tariff rates, ranging from 13% to 50%, were previously planned to take effect on April 9 for around 60 nations, including Thailand, that has a significant trade surplus with the US. However, the US announced a 90-day pause of the reciprocal tariffs but has still imposed the 10% global tariff.

-

Under the reciprocal tariff, ASEAN nations would be broadly affected, with the highest tariff rates imposed on Cambodia (49%), followed by Lao PDR (48%), Vietnam (46%), Myanmar (44%), Thailand (previously announced at 36%, later revised to 37%, and now corrected back to 36%), and Indonesia (32%). Several ASEAN economies exhibit significant export dependency on the US market, with Cambodia leading at 38% of its total exports, followed by Vietnam (28%), Thailand (17%), and the Philippines (15%). Regarding the world’s major countries, the hardest hit is China, facing a 145% tariff, followed by India (26%), South Korea (25%), Japan (24%), and the European Union (20%).

-

The new reciprocal tariff rates are higher than our previous estimate, as the method used by the US is different from what they previously announced, i.e., only considering differences in MFN tariff rates, Value Added Tax (VAT) rate, currency manipulation, and non-tariff barriers.

Short-term impact of reciprocal tariffs could push Thai exports to near zero growth; Losses could have negative spillover, hurting from agricultural to manufacturing sector

Economic scenarios: Twin shocks from March earthquake and US tariff hikes may have significant impacts on Thai economic outlook

In the long term, US and global economies will face largest GDP and export losses from tariff hikes; Thailand and ASEAN will suffer net losses if reciprocal tariffs are imposed

Scenario 1: US imposes a 10% tariff on most countries and a 145% tariff on China. China retaliates with a 125% tariff on US goods.

Scenario 2: US imposes the announced reciprocal tariffs on many countries and a 145% tariff on China. China retaliates with a 125% tariff on US goods.

Most Thai industries face long-term losses from tariff hikes and surging imports from China. Some sectors may see a positive substitution effect, investment relocation, or export rerouting

Scenario 1: US imposes a 10% tariff on most countries and a 145% tariff on China. China retaliates with a 125% tariff on US goods.

Scenario 2: US imposes the announced reciprocal tariffs on many countries and a 145% tariff on China. China retaliates with a 125% tariff on US goods.

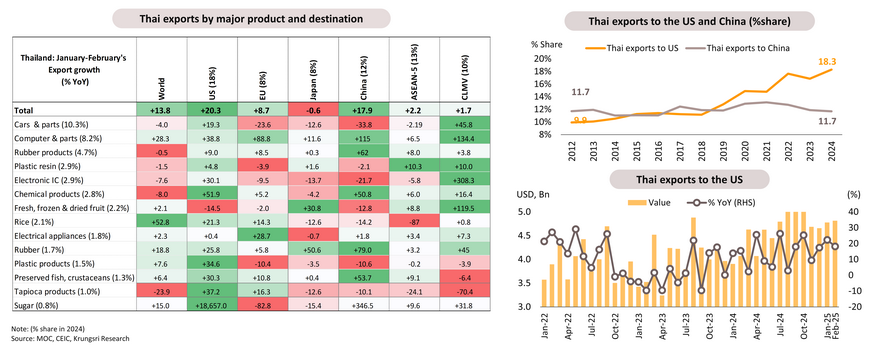

Export growth holds up in February, but with temporary demand amid concerns over tariff hikes

Despite a 90-day pause of reciprocal tariffs, high uncertainties over US trade policy, negotiation result, and flooding Chinese goods cloud export outlook

In the first two months of 2025, Thai exports grew 13.8% YoY (based on MOC data), led by Industrial products, which expanded by 17.1% (including computers & components, plastic products, and electrical appliances), agro-industrial products which expanded by 6.7% (such as canned & processed seafood, pet food and sugar). However, exports of agricultural products decreased by -1.9%, led by rice and fresh, chilled, frozen & dried fruit. Also, exports of cars and parts continued to contract. Rising global trade tensions, driven by the US imposing a 10% baseline tariff on most imports (including from Thailand) effective April 5, and a pending 36% reciprocal tariff on Thai goods, are clouding the export outlook. Despite a 90-day delay in enforcement, exporters’ concerns remain high. Thailand’s export growth for 2025 is now likely to fall short of our earlier 2.7% forecast.

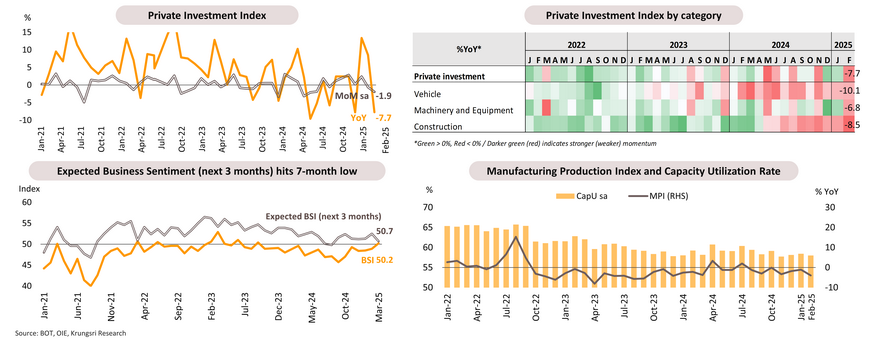

Private investment lost momentum, facing ongoing pressure from structural problem, earthquake impact, and global trade challenges

In February, the Private Investment Index contracted by -7.7% year-on-year and declined by -1.9% MoM sa. Investment in machinery and equipment declined again, in line with a drop in imports of capital goods. Vehicle investment dropped, mainly due to a decline in passenger car production. Meanwhile, construction continued to contract, in line with the sluggish real estate market. The private investment is facing increasing headwinds, including structural challenges and intensifying global trade tensions. As a result, some businesses may delay investment decisions while awaiting clearer signals on trade policies from major economies, which could dampen foreign direct investment inflows into Thailand. In addition, despite rehabilitation spending in response to the March earthquake, the weaker outlook of the property sector could also adversely affect business investment.

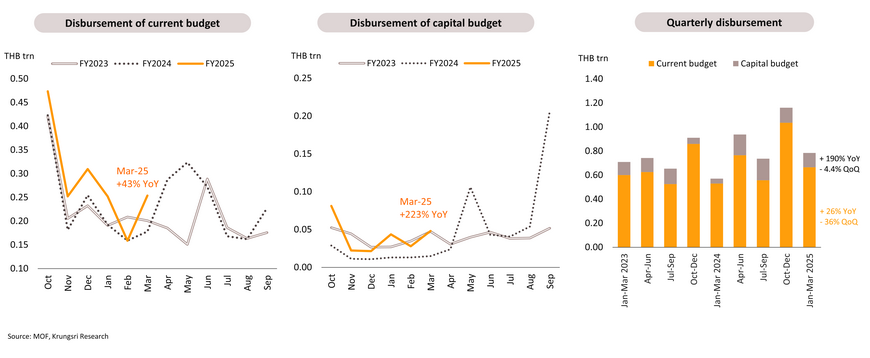

Government spending remains a key growth driver in 1Q25; disbursements are likely to normalize going forward

Preliminary data from the Ministry of Finance showed that disbursement of the current budget increased by 43% YoY in March and disbursement of the capital budget surged by 223%. In the first half of FY2025 (October 2024 to March 2025), disbursement of the current budget increased 22.4% YoY to THB 1.7 trn, accounting for 61% of the annual budget. For the capital budget, the government’s disbursement surged by 165% YoY to THB 0.24 trn, accounting for only 25% of the annual budget. In the second quarter of FY2025 (January-March), total budget disbursement expanded by 37.4% from the same period last year but declined by -32.4% from the previous quarter.

Service sectors and short-term stimulus helped lift private consumption early this year, but the outlook remains under pressure

In February, the private consumption index (PCI) grew by 2.6% YoY, supported by growth in the services category. Key drivers included (i) the recovery of the tourism and other service sectors, and (ii) short-term stimulus measures.

However, the outlook for private consumption may weaken due to (i) a continued decline in consumer confidence in response to the March earthquake; (ii) downside risks to the Thai economy due to US tariff hikes and escalating trade tensions between the US and China; (iii) sluggish income growth, as reflected by the average real income in 2024 which increased by only 3.2% compared to pre-COVID levels (in 2019); (iv) a slowdown in agricultural income due to price-related factors; and (v) persistently high household debt.

Household debt slowed to 88.4% of GDP in 4Q24, mainly due to a contraction in automobile loans

Thailand’s household debt edged up only 0.2% YoY in 4Q24, while the household debt-to-GDP ratio continued to decline, reaching 88.4%, the lowest level since 3Q20. The slowdown in household debt was mainly driven by a contraction in auto loans, credit card loans, and personal loans, while real estate loans also showed signs of deceleration. In terms of debt quality, non-performing loans (NPLs) at Thai commercial banks stood at THB 496.1 bn in 4Q24, accounting for 2.71% of total loans vs 2.66% at end-2023. For consumer loans, credit-card NPLs increased from 3.57% of total loans at end-2023 to 3.83% at end-2024. Real estate NPLs rose from 3.34% to 3.88% in the same period. Auto loan NPLs remained steady at 2.13% but could rise in the coming period. This trend is reflected in the Significant Increase in Credit Risk (SICR or Stage 2) group, which remained elevated at 15.6% of total loans at end-2024 from 14.29% at end-2023.

March inflation softened to below the BOT’s 1-3% target range, and full-year average likely to be less than our 1% forecast

Forward guidance on policy rate: BOT assesses that the current US tariffs hit “some” sectors and requires supply-side policy as a remedy, increasing the likelihood of a dovish hold this month

MPC is expected to adopt a wait-and-see stance in April, but rising downside risks raise the chance of rate cuts later this year