Escalation of trade protection measures adds pressure on economic recovery in major countries; China faces risks on multiple fronts.

US

.

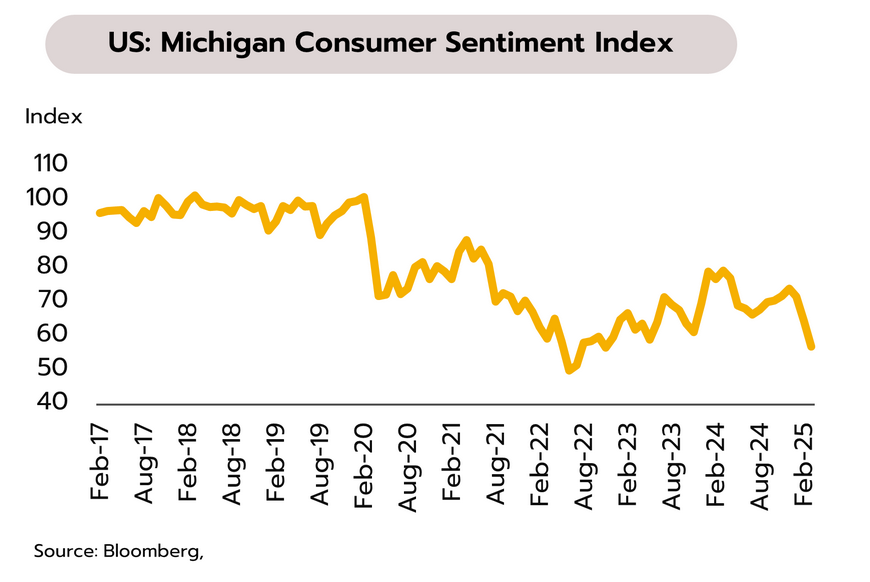

US economy faces risk of slower-than-expected growth as Trump imposes 25% auto tariffs. In March, the economy showed signs of weakening, with the Flash Manufacturing PMI slipping into a contraction zone at 49.8, while the Flash Services PMI improved to 54.3. However, consumer confidence dropped to 57, its lowest level since November 2022.

The trade war escalation has heightened concerns about a sharper-than-expected US slowdown due to higher import costs and weaker employment. This concern was reflected in the US stock market, which fell over 3% last week amid worries about reciprocal tariffs and 25% tariffs on all cars not manufactured in the US, to take effect on April 3. Such developments could trigger countermeasures from trading partners, adding risks to trade and economic growth. Given these factors, Krungsri Research expects the Fed to cut the policy rate three times this year, by 25bps each, bringing it to 3.50%-3.75% by year-end, with the first cut likely in mid-2025.

Japan

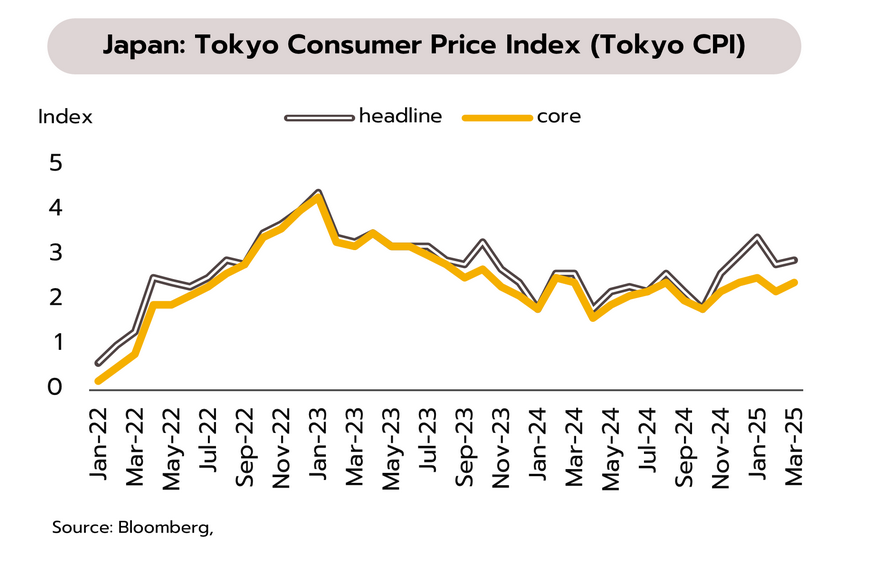

Japan’s recovery faces mounting challenges as inflation remains elevated and trade tensions escalate. In March, the Flash Manufacturing PMI declined to 48.3, while the Services PMI unexpectedly fell into contraction at 49.5. Inflationary pressures remained, with Tokyo’s headline inflation rising from 2.8% YoY in February to 2.9% in March, while core inflation climbed from 2.2% to 2.4%.

Japan's recovery faces mounting pressure from high inflation and escalating trade wars following US president Trump's announcement of 25% tariffs on car imports. This measure is expected to have a significant impact on Japan's economy, as car exports accounted for 28.3% of Japan’s total exports to the US in 2024. Japan has stated that it is considering negotiations to address the issue while keeping open the possibility of retaliatory measures against the US. Despite still-high inflation, Japan’s recovery remains sluggish, suggesting that the BOJ is in no rush to raise its policy rate, with a hike likely in the second half of the year.

China

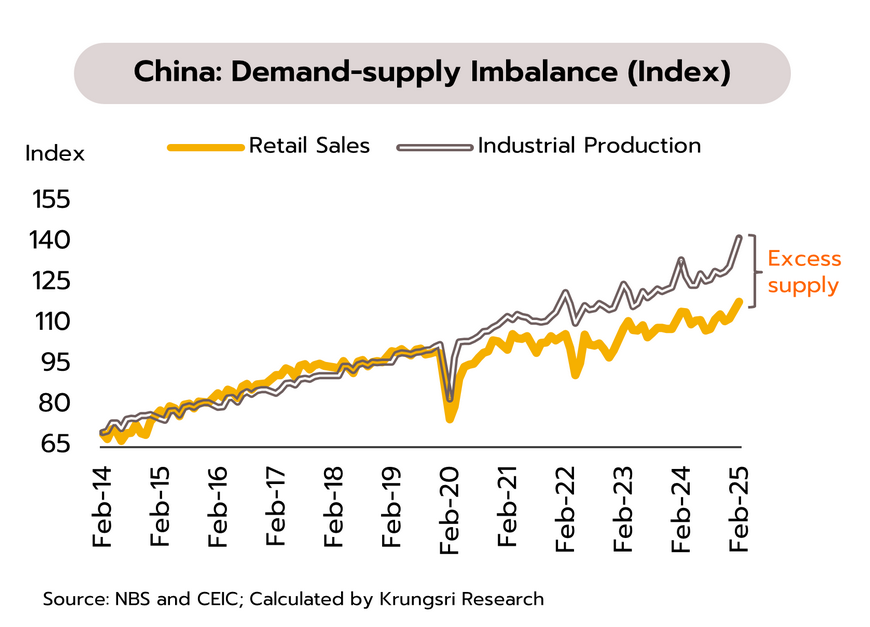

China’s domestic economy remains fragile, while external risks from trade wars are intensifying. Industrial profits contracted by -0.3% YoY in January–February, down from +11% in December. This aligns with retail sales, which grew by only 4%. Meanwhile, the gap between industrial production index and retail sales index has significantly widened from pre-COVID levels during 2014-2019 (see chart).

These indicators highlight headwinds for the economy, ranging from oversupply in several industries and weak purchasing power. Moreover, export growth has slowed noticeably (2.3% in January–February vs 6-11% in 4Q24). Recently, the US announced 25% tariff hikes on auto imports, effective April 3. Our study found that its impact on China would be limited, with exports expected to decline by 0.32% from the baseline. However, if the US imposes tariffs on auto parts, the impact could be more severe.

US reciprocal tariffs and slow tourism recovery pose key challenges for Thailand’s economic outlook

February economy boosted by a temporary rebound in export growth, while private spending slows down. The Fiscal Policy Office (FPO) reported that Thailand's economy in February was supported by merchandise exports, which continued to grow sharply by 14% YoY. However, in the tourism sector, the number of international tourist arrivals to Thailand slowed to 3.12 mn (-6.9% YoY). Private consumption growth showed signs of deceleration, mainly due to a decline in durable goods spending. Similarly, private investment growth weakened, as reflected by a drop in capital goods imports compared to the same month last year. This aligned with industrial production, which contracted at a faster rate by -3.9% in February.

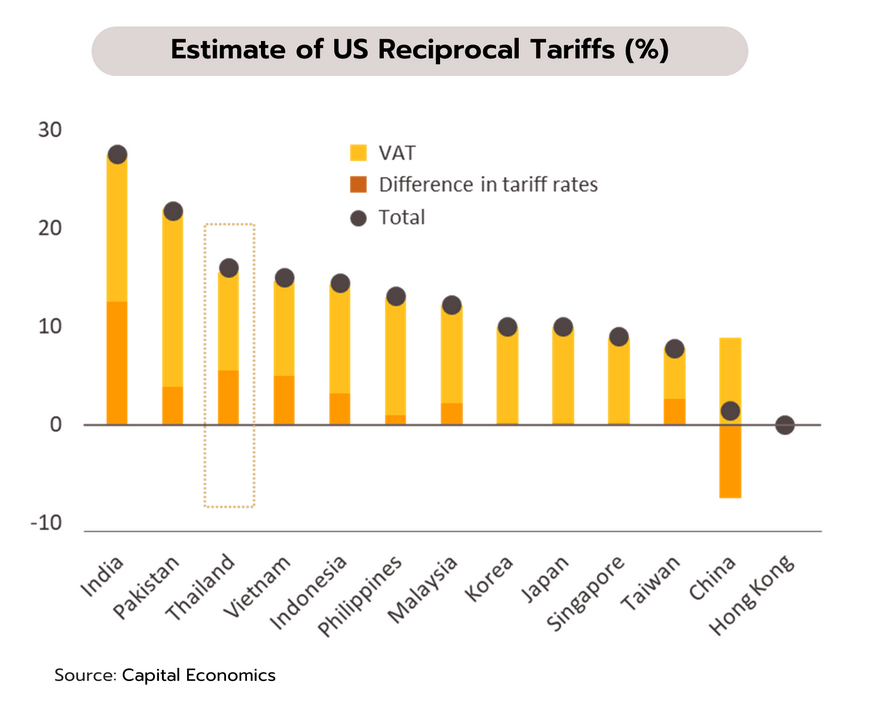

The outlook for the Thai economy remains clouded by uncertainty and risks stemming from US trade measures, which could threaten the export growth, a key economic driver in early 2024. Recently, the US announced an increase in import tariffs on automobiles by 25%, effective April 3. Although the direct impact on Thailand may be limited, as Thai car exports to the US account for only 1.6% of total Thai car exports, it is estimated that the move could reduce Thailand’s overall exports by around -0.05%. Moreover, if the US proceeds with serious implementation of reciprocal tariffs against countries with trade surpluses, Thailand is among those at high risk of being targeted. This could further affect Thai exports and manufacturing for the remainder of the year. Thailand’s average tariff rate is 5-6% higher than that of the US, and with the country’s VAT rate at 7%, US reciprocal tariffs on Thai goods could reach as high as 13%, which could be the highest among ASEAN countries.

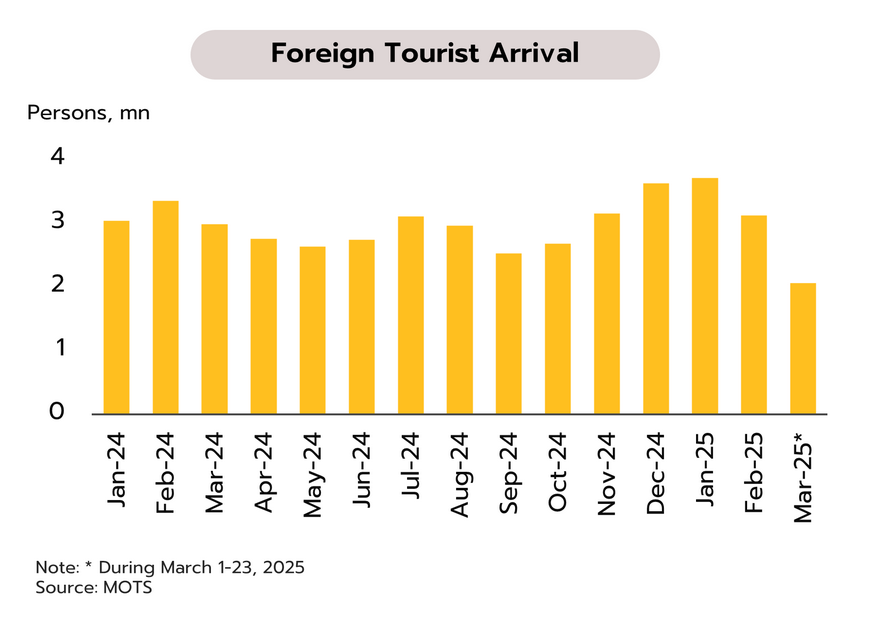

Government plans to boost domestic tourism amid concerns over short-term impact from earthquake. The latest tourism situation shows that between January 1 and March 23, Thailand welcomed 8.89 mn foreign tourists, a 2.9% increase year-on-year, generating THB434.66 bn in revenue. The top source markets were China (1,259,391 persons), Malaysia (1,057,438), Russia (667,905), India (498,341), and South Korea (475,124). As for domestic tourism, during the first two months of this year, there were 16.48 mn-trips (+4.1% YoY), generating THB 8.8 bn in revenue (+6.6%).

To help support a further recovery of the tourism sector following a slow return of Chinese tourists, the Ministry of Tourism and Sports recently revealed that it is considering launching a new phase of the “We Travel Together” campaign during the low season (after the Songkran Festival). The preliminary plan includes 1 mn participants, with a maximum subsidy of THB 3,000 per person. The government will cover 40% of expenses for travel to major cities and 50% for secondary cities (excluding airfare). Additionally, the ministry is considering extending the visa-free policy for Chinese tourists but may reduce the allowed stay from 90 days to 30 days, as most visitors typically stay for 10–15 days. Meanwhile, the impact of the recent earthquake is still being assessed, and it could potentially affect tourism sector, business and consumer sentiment, as well as overall economic activity. Initially, the Association of Thai Travel Agents (ATTA) and the Thai Hotels Association (THA) said that the short-term impact on Thailand's tourism industry would stem from safety concerns. They expected that the number of international tourists to drop by 10%-15% or even more in the next two weeks.