Key takeaways: Business opportunities in the Philippines are ample despite some structural challenges

- The Philippines economy is facing both internal and external challenges in the near term. As a result, growth is expected to expand by 5.0% in 2023 and by 6.0% in 2024, according to the IMF (as of January 2023). Rising inflation compounded by tightening domestic financial conditions will hurt domestic consumption and investment, and a darkening global economic outlook will dent the external demand. However, in the longer term, we expect the economy to gradually rebound to its potential growth trajectory of 7% p.a. supported by its favorable fundamentals, infrastructure investment, and ongoing structural reforms.

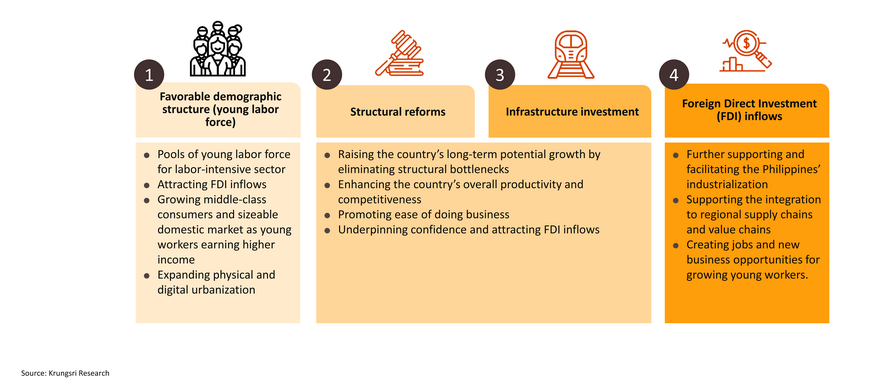

- In the medium to longer term, despite some structural challenges, we remain optimistic about the potential of the Philippines economy as there are relatively favorable fundamentals compared to regional peers and this would help the country to secure its high potential growth path in the years to come. Key fundamentals to drive the economy are (1) demographic dividend, (2) structural reforms, (3) infrastructure investment, and (4) FDI inflows. This opens up business opportunities for foreign investors in some of the potential sectors including food and beverage, beauty and personal care, tourism, and agriculture.

Philippines: A Country Overview

Geographically, the Philippines economy will continue to be dominated by the NCR, Calabarzon, and Central Luzon region

Macro forecasts: The pandemic’s scar remains visible in the medium term, but the long-term outlook is still promising

The main economic engines are recovering from the pandemic-caused slump in 2020; surging inflation poses challenges to the near-term outlook

Inflation has reached a 14-year high, driven by high prices of food and utility; the above-target inflation is likely to be contained as policy interest rate has been raised aggressively

Rising debt and twin deficits are also likely to complicate the recovery in the medium term

Major milestone of the Philippines’ socioeconomic developments

Structure and Potentialof the Philippines Economy

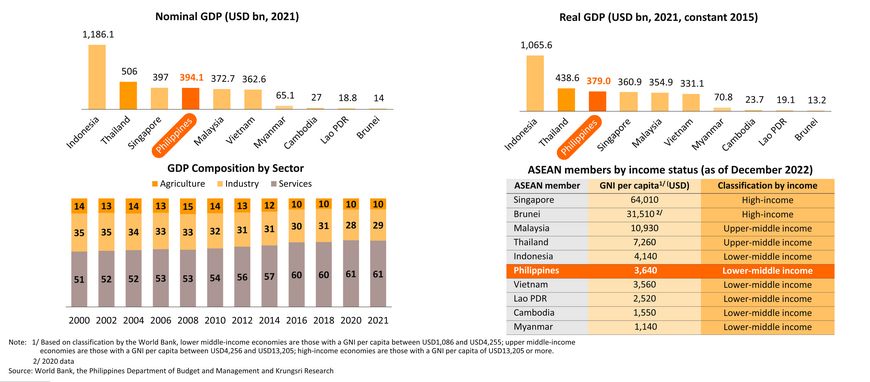

Philippines among ASEAN peers: achieving upper-middle income country status by 2023 is unlikely

The Philippines is still classified as a low-middle income country, with a GNP per capita of USD 3,650 in 2021. Although the Philippines experienced relatively high economic growth of 6.4% on average from 2010 to 2019, and its economy has been shifting toward higher-value-added sectors over the past two decades, President Ferdinand Marcos Jr.'s optimistic expression on achieving upper-middle income status by 2023 is still unlikely. According to its Department of Budget and Management and our projection, GNP per capita will be around USD 4,075 in 2023, falling slightly short of the upper-middle income group's lower bound.

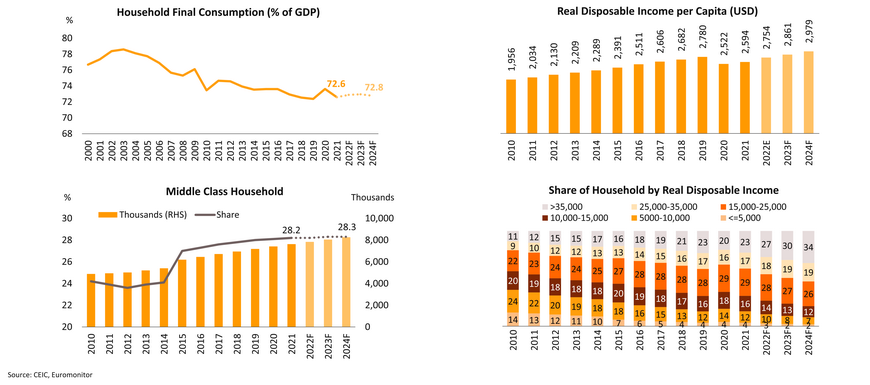

Household spending will continue to serve as a major economic engine for many years to come

Household consumption accounted for 72.6% of GDP in 2021 and is expected to rise to 72.8% by 2024. Despite high global inflation, real per capita disposable income is recovering and is expected to surpass pre-pandemic levels by the end of 2023. Meanwhile, the middle class has gradually expanded. By 2024, most households will have real disposable incomes of more than USD 25,000. Therefore, domestic consumption will continue to play a crucial role in driving economic growth in both medium and long term.

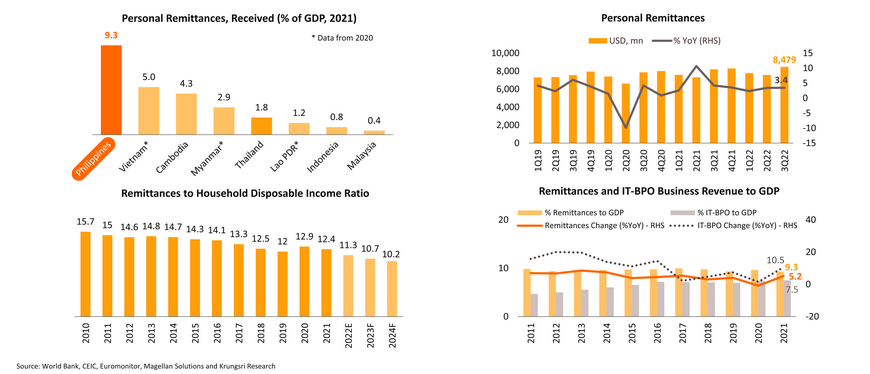

Remittance is also likely to remain a crucial source of income, but its influence is gradually fading

Among ASEAN peers, the Philippines has the highest remittance-to-GDP ratio, accounting for nearly 10% in 2021. After recovering from a slump during the first phase of Covid-19 in 2020, remittance has continued to rise. However, its significance in sustaining Filipino household income is dwindling. In 2024, it is predicted to account for 10.2% of disposable household income. Meanwhile, revenue from working in IT Business Process Outsourcing (IT-BPO) is rising sharply and is expected to outpace remittance in the coming years due to a surge in demand.

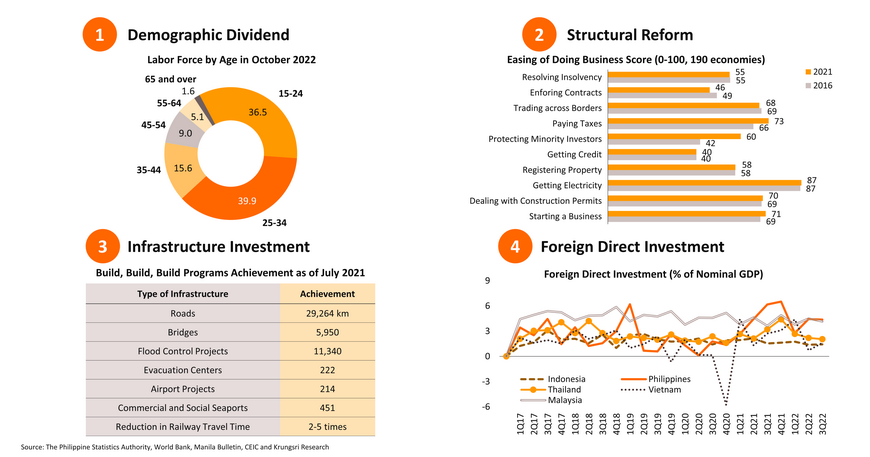

The labor market is still recovering from the pandemic’s peak and likely to improve further in 2023; by 2032, the Philippines will not bear much of the burden from an aging society

Favorable population structure, large pool of labor force with moderately high productivity and low minimum wages provide comparative advantages in labor-intensive sectors

…however, investors should carefully weigh their options since regional and industry-specific minimum wages vary

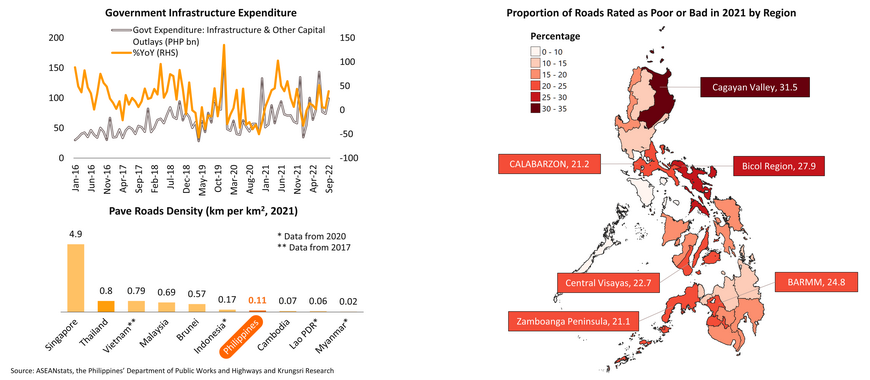

...as well as the quality of the common transportation system, particularly roads which lag behind its neighbor

To address the country's enduring infrastructure gaps, the Duterte administration launched the "Build, Build, Build" program in 2017. Despite efforts, the most basic mode of transportation appears to improve only in terms of coverage (unpaved roads decreased from 8.4% of total road length in 2016 to 1.4% in 2021), not quality. Furthermore, the Philippines' road density continues to lag behind its peers. As the new government promises to continue and expand previous infrastructure programs, we expect that overall infrastructure will continue to improve significantly over the next six years.

In the last decade, the Philippines has mainly attracted investment from Singapore, the Netherlands, and Japan, with manufacturing sector receiving the most attention; geographically, CALABARZON is still the most appealing region

A more liberal exchange rate policy and a lower CIT could contribute to a more favorable investment environment

...which would also benefit from the revised business law; however, this could be complicated by restrictions on foreign ownership control and widespread corruption

Exports continue to be heavily reliant on the electronics and machinery, as well as ICT services; Imports, on the other hand, are much more diverse; China remains the largest trading partner

The Philippines remains one of the key trading partners in ASEAN for Thailand

Despite the obvious scars left by the pandemic and high inflation, strong fundamentals could help the country get back on track in the long run

Although the Philippines has gradually recovered from the worst of the pandemic, high inflation, rising debt, and worsening twin deficits will likely limit economic growth in the coming years to

5-6%, less than the pre-pandemic five-year average of 6.6%. We expect the Philippines' economy to resume its potential trajectory and effectively address long-standing structural challenges in the long term as a result of the four main factors listed below: (1) demographic dividend, (2) structural reforms, (3) infrastructure investment, and (4) FDI inflows.

Business Opportunities in the Philippinesfor Thailand

Sizeable domestic demand and growing wealthier middle-class Filipino consumers offer business opportunities for Thai investors

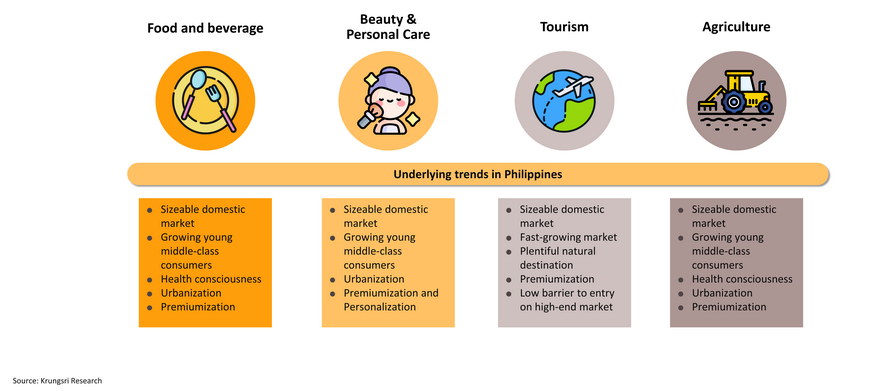

The Philippines' population will be around 133 million by 2032. Because of the high rate of economic growth, this would imply a large number of young and wealthy consumers. Looking ahead, the Philippines should continue to be one of the most thriving economies in the region, providing opportunities for Thai companies seeking to expand their operations. According to our analysis, the potential sectors are food and beverage, beauty and personal care, tourism, and agriculture.

Food: Thailand’s food expertise will provide Thai investors a leg up on the competition; however, high-end healthy food market is still niche and dominated by few companies

Beverage: Although Filipinos continue to enjoy alcoholic beverages, the demand for healthier alternatives is increasing and expected to accelerate in the long term

Beauty and Personal Care1/: Demand quickly recovering from the pandemic’s slump will resume its potential trajectory in 2023-2024, and maintain high growth in the long run

….owing primarily to a growing middle class of wealthier consumers and a premiumization trend; newcomers are likely to have better chances of competing in the Philippines

Tourism: With the country reopening in 2021, demand and spending are expected to surge in 2023, eventually surpassing the pre-pandemic level in the coming years

Abundant natural attractions and a lack of high-end hotels present an excellent opportunity; however, high market concentration and high crime rates remain challenging

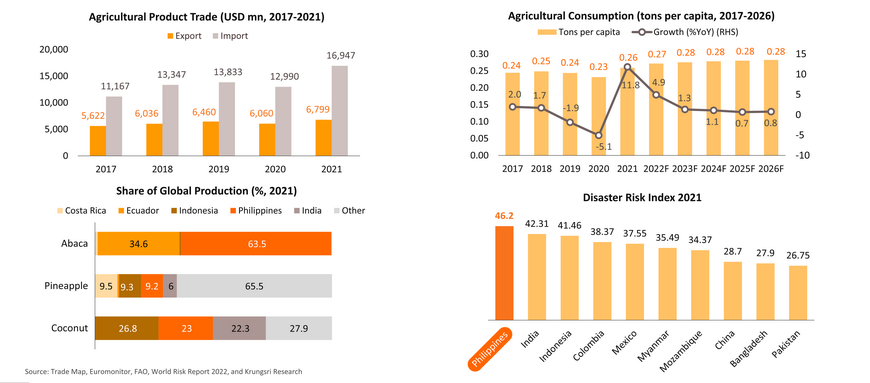

Agriculture: Demand is rising in tandem with the population growth, necessitating a reliance on imports

The Philippines has been a net importer of agricultural products for many years, and this trend is expected to continue as per capita consumption remains stable at 0.28 tons. This should present an excellent opportunity for Thai investors in two scenarios: (1) an increase in fresh or processed product exports, and (2) direct investment. The latter scenario is supported by the fact that the Philippines is a major producer of certain crops that could be used to manufacture a wide range of foods or materials. The Philippines, however, is the most disaster-prone country in the world.